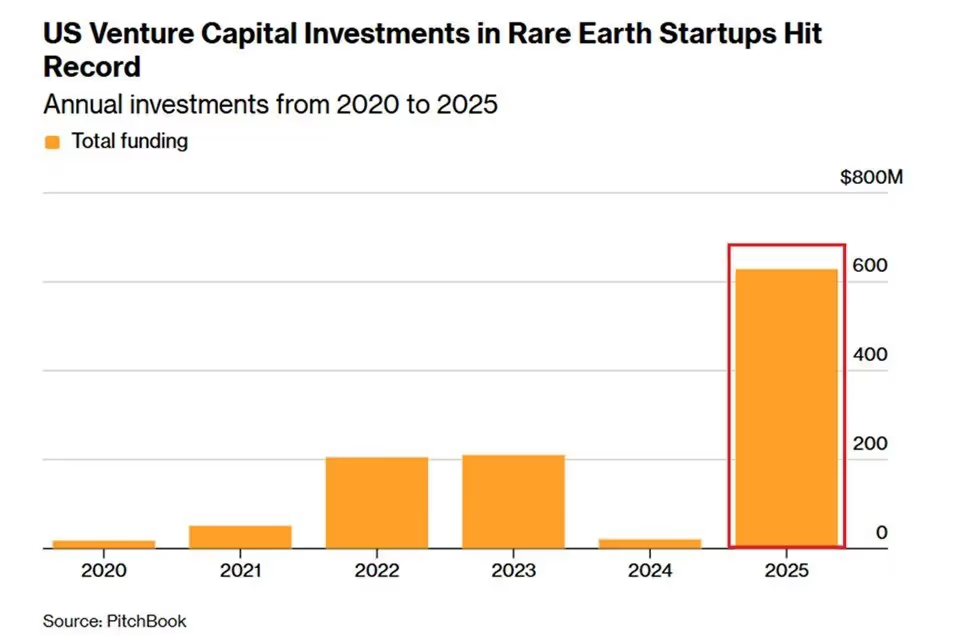

U.S. venture capital investment into rare earth mineral startups reached $628.5 million in 2025, the highest annual total ever recorded for the sector. That figure represents a near 3,000% increase from 2024, according to industry funding data, and accounts for roughly 90% of global venture funding directed at rare earth projects last year. Importantly, these numbers exclude direct government investments, including a $400 million equity injection by the U.S. Department of Defense into MP Materials in July 2025.

This is not a typical commodity cycle story. It is a capital allocation response to geopolitical exposure. China currently controls around 60% of global rare earth mining output and over 90% of refining capacity, a concentration that has become increasingly uncomfortable for U.S. policymakers as supply chains collide with defense, energy transition, and technology priorities.

The capital inflows signal something structural. Venture investors are no longer treating rare earths as a niche materials bet. They are treating them as a strategic bottleneck problem with state backing, long time horizons, and limited global alternatives.

Why Rare Earths Suddenly Moved From Obscurity to Priority

Rare earth elements are essential inputs for permanent magnets, electric vehicle motors, wind turbines, advanced electronics, and defense systems. For decades, Western economies accepted Chinese dominance because supply was reliable and prices were low. That calculus has changed.

China has repeatedly signaled its willingness to weaponize critical minerals policy during periods of trade or geopolitical tension. Export controls on gallium and germanium in 2023 served as a warning shot. Rare earths sit higher on the escalation ladder because there are few near-term substitutes and limited refining capacity outside China.

According to U.S. Geological Survey data, China's mining share hovers near 60%, but its refining dominance exceeds 90%, creating a choke point that mining projects alone cannot fix. Refining, separation, and downstream processing are where most projects fail to scale economically. That is why capital is flowing not only to miners but also to processing technology startups and vertically integrated models.

This context explains why venture funding surged even before government dollars were counted. Investors are positioning ahead of long-term policy guarantees, not chasing short-term price spikes.

Venture Capital Fills Gaps Government Funding Cannot Reach

The $628.5 million in VC investment does not include government-backed transactions. That distinction matters. State funding tends to target established players, while venture capital targets process innovation, early-stage extraction technologies, and modular refining approaches that legacy miners avoid.

The Pentagon's $400 million equity investment in MP Materials focused on securing supply for defense needs. Venture capital, by contrast, is flowing into startups attempting to solve cost, scalability, and environmental barriers that have historically kept rare earth projects uncompetitive outside China.

This split creates a layered capital structure. Government capital anchors demand certainty. Venture capital absorbs technical risk. Together, they shorten timelines that would otherwise stretch over decades.

Industry tracking from IndexBox shows that U.S. startups captured the overwhelming majority of global rare earth venture funding in 2025, a sharp reversal from previous years when capital was scattered across Australia, Canada, and Southeast Asia.

The China Dependency Problem Is Larger Than Mining Volumes

Focusing only on mining understates the challenge. Rare earth separation is chemically complex, environmentally sensitive, and capital intensive. China's dominance was built through decades of state support, regulatory tolerance, and integrated supply chains.

Western projects face higher compliance costs, stricter environmental standards, and fragmented demand. Venture capital is stepping into this gap by funding process efficiency rather than brute-force scale.

Bloomberg reporting highlights that more than 90% of global rare earth refining still occurs in China, even when ore is mined elsewhere. Until refining capacity diversifies, supply risk remains embedded in the system.

This reality explains why investors are backing companies that look less like miners and more like advanced materials firms. The value is in control of processing, not extraction alone.

Counterargument: Capital Alone Does Not Solve Structural Constraints

There is a real risk of overestimating what venture capital can fix. Rare earth projects remain exposed to commodity price volatility, permitting delays, and long development timelines. Even with record funding, bringing new refining capacity online takes years.

There is also execution risk. China's cost advantage is structural, not accidental. Higher labor costs, environmental compliance, and energy prices in the U.S. mean many projects will struggle without continued policy support.

Some analysts argue that without long-term offtake agreements or price floors, venture-backed startups may fail once geopolitical urgency fades. Capital inflows today do not guarantee sustainable production tomorrow.

This skepticism is healthy. It reinforces why the current surge should be viewed as a strategic hedge rather than a guaranteed supply chain solution.

What This Means for Markets Going Forward

The rare earth funding surge reflects a broader shift in how markets price geopolitical risk. Supply security is becoming an investable theme, not just a policy concern.

For investors, this does not translate into simple commodity exposure. It favors companies positioned at choke points: refining, separation, and magnet manufacturing. It also suggests that future volatility will be policy-driven rather than demand-driven.

For policymakers, the data sends a clear message. Private capital will move when incentives align, but it cannot replace long-term industrial strategy. The U.S. is buying optionality, not independence, at least for now.

The key takeaway is not that rare earth shortages are imminent. It is that capital is re-pricing supply concentration risk in real time.

The record $628.5 million venture capital inflow into U.S. rare earth startups in 2025 is not a speculative anomaly. It is a rational response to supply concentration, geopolitical signaling, and industrial vulnerability. China's control over mining and refining has transformed rare earths from a materials footnote into a strategic priority.

Venture capital is stepping in where markets failed to price risk for decades. Whether that capital ultimately delivers durable supply diversification remains uncertain. What is clear is that rare earths have crossed a threshold. They are no longer just commodities. They are leverage points.

.png)