Wall Street has officially rewritten the record books.

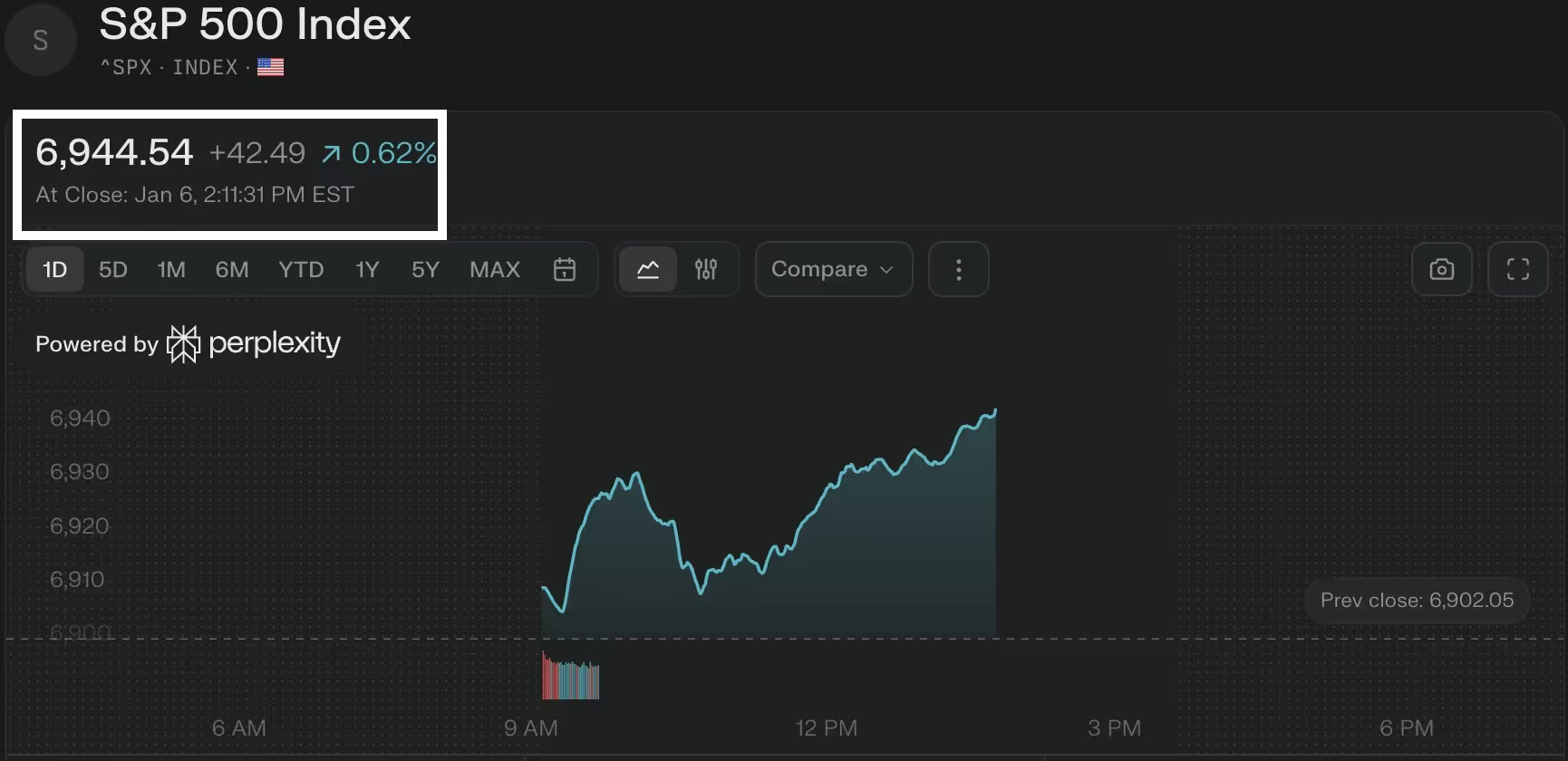

On January 6, the S&P 500 closed at 6,944 points, marking a new all-time high and extending one of the most aggressive rallies of the past decade. From its April 2025 low, the index is now up roughly 44%, a recovery that has caught even optimistic investors off guard.

Just nine months ago, the dominant narrative was very different. Markets were grappling with stubborn inflation, restrictive monetary policy from the Federal Reserve, and fears that elevated interest rates would eventually choke off corporate earnings. Calls for a structural downturn were widespread.

Instead, the S&P 500 not only recovered, it pushed decisively into uncharted territory. The move matters not because it is another green day on the chart, but because it forces a reassessment of where the U.S. equity market truly stands heading into 2026.

From April Panic to January Euphoria

The April 2025 lows marked a moment of genuine stress. Equity valuations were compressing, rate-cut expectations were being pushed further out, and earnings growth was under scrutiny. At that point, positioning across institutional portfolios had turned defensive.

What followed was not a single catalyst, but a gradual re-acceleration driven by a narrow yet powerful group of forces. Mega-cap technology stocks regained leadership, capital rotated back into growth, and investors slowly rebuilt risk exposure.

According to Bloomberg market data, the magnitude of the rebound places this rally among the strongest post-drawdown recoveries of the last twenty years. The speed of the move, rather than just the size, is what stands out.

Technology and AI Remain the Engine

The current all-time high is inseparable from the continued dominance of large-cap technology. Semiconductor leaders like NVIDIA, cloud infrastructure providers like Microsoft and Amazon, and companies tied to artificial intelligence have once again acted as the market's backbone.

According to FactSet earnings data, expectations for AI-driven revenue growth remain embedded in forward guidance across multiple sectors. Investors appear willing to pay a premium for companies perceived as structural beneficiaries rather than cyclical winners.

This concentration, however, comes with trade-offs. Market breadth has improved compared to early 2025, but leadership remains narrow by historical standards. A large portion of index-level gains is still driven by a relatively small number of names. That makes the rally powerful, but also fragile.

Valuations Are No Longer a Side Issue

At current levels, valuation concerns can no longer be dismissed as background noise.

According to CAPE ratio data and Yardeni Research forward P/E tracking, the S&P 500's forward price-to-earnings ratio is now comfortably above its historical average. This does not automatically imply an imminent correction, but it does mean that expectations are high and margin for error is thin.

In practical terms, the market is priced for continued earnings resilience, controlled inflation, and a gradual easing of financial conditions. Any deviation from that path, whether through weaker earnings or macroeconomic shocks, would be felt more sharply at these levels.

This is the cost of a fast recovery. The upside has already been pulled forward.

The Counterargument for Why Momentum Still Matters

Despite valuation concerns, dismissing the rally outright would be a mistake.

According to S&P Global historical market analysis, sustained all-time highs often coincide with periods of strong momentum rather than immediate reversals. Markets do not typically peak quietly. They tend to exhaust themselves through failed breakouts, deteriorating breadth, or sharp liquidity stress. None of those signals are clearly present yet.

Liquidity conditions, while not loose, have stabilized. Corporate balance sheets remain resilient, and buybacks continue to provide structural support. According to Goldman Sachs equity strategy research, betting aggressively against the trend has proven costly throughout this cycle.

The market may be expensive, but it is not obviously broken.

What This Rally Tells Us About 2026

The most important takeaway from the S&P 500's record close is not the number itself, but the message behind it.

Markets are signaling confidence in earnings durability and a belief that the macro environment, while imperfect, is manageable. That does not guarantee smooth sailing, but it does suggest that fears of an imminent collapse are not currently shared by capital allocators.

At the same time, the rally has created a more asymmetric setup. Upside from here likely requires continued execution rather than narrative expansion. Downside risks have grown sharper simply because prices are higher. This is no longer a market that forgives disappointment easily.

As 2026 begins with a fresh all-time high, the central question is unavoidable: Is this the late stage of an extended bull market, or the foundation for another leg higher? Both scenarios remain plausible. What is clear is that the market has chosen momentum over caution for now.

The S&P 500 is not hesitating. Whether the market can sustain this pace without broader participation and earnings follow-through will determine how this chapter ends. History is being written. The margin for error is narrowing.

.png)