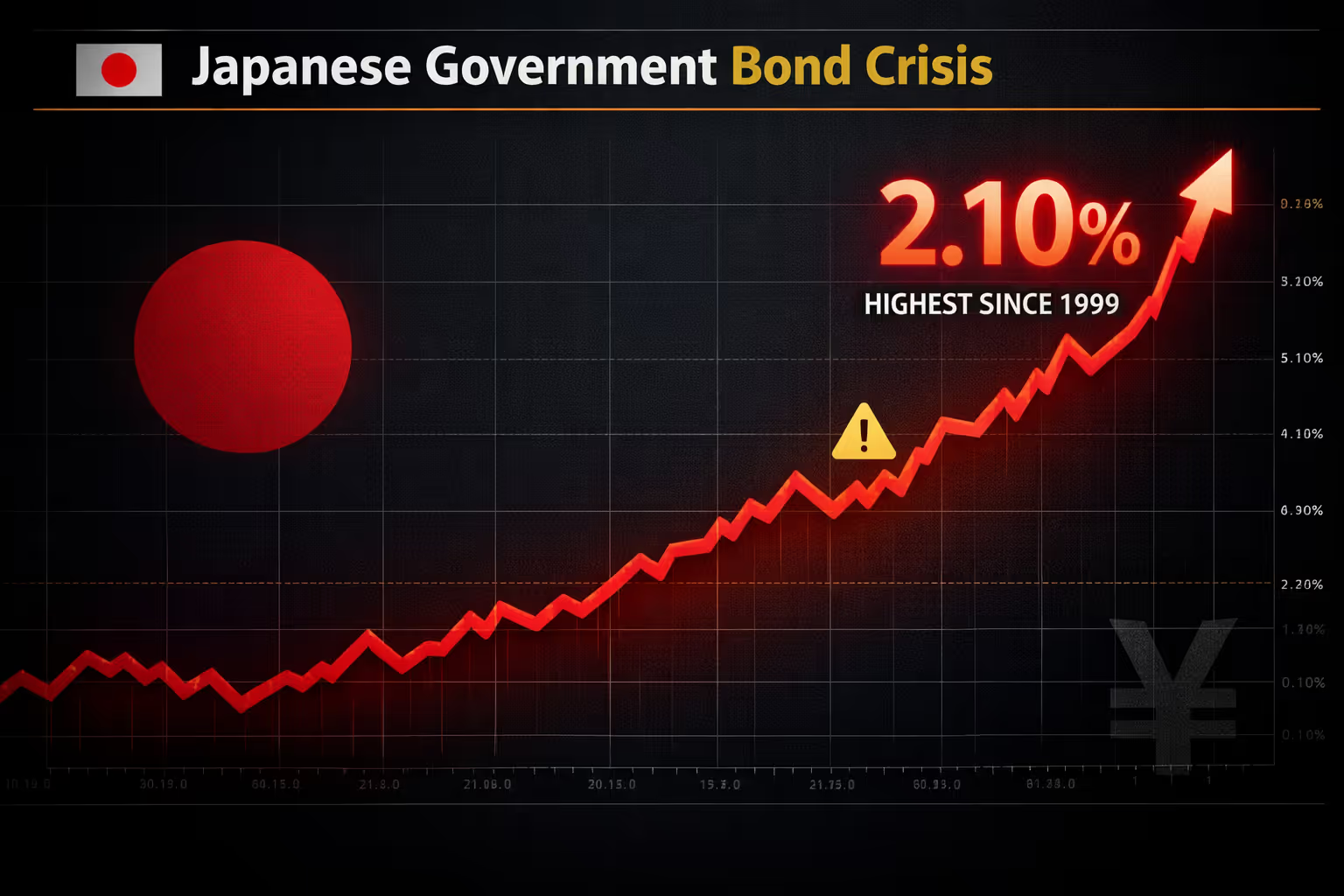

Japan's 10-year government bond yield surged to approximately 2.10% in December 2025, marking the highest level since 1999 and representing nearly 100 basis point increase over the past year. The move follows Bank of Japan's continued policy normalization, rising inflation expectations, and weakening yen forcing investors to demand higher term premium for holding Japanese government debt.

The surge matters because Japan operates under fundamentally different fiscal constraints than typical developed economies. With government debt exceeding 250% of GDP according to IMF data—highest among major economies—rising yields translate directly into ballooning debt-servicing costs that threaten fiscal sustainability. What functioned under zero and negative rate environment becomes unsustainable when yields approach historical norms.

Why 2.10% Represents Structural Inflection Point

The 2.10% level carries significance beyond nominal rate. Japan's last sustained period above 2% occurred during late 1990s before Bank of Japan implemented zero interest rate policy in 1999. The subsequent 25 years of ultra-low rates allowed Japan to finance massive debt loads without triggering fiscal crisis. Debt-servicing costs remained manageable despite climbing debt-to-GDP ratio because rates stayed suppressed.

The arithmetic changes dramatically at 2%+ yields. Japan's outstanding government debt totals approximately ¥1,200 trillion ($8 trillion) as of 2025. Each 100 basis point increase in average borrowing costs adds roughly ¥12 trillion ($80 billion) in annual interest expense. When yields move from 0% to 2%, debt-servicing doubles from already elevated levels even before accounting for new issuance.

The Bank of Japan owns approximately 50% of outstanding Japanese government bonds through quantitative easing programs implemented since 2013. This ownership provided artificial demand keeping yields suppressed even as debt levels climbed. As Bank of Japan signals policy normalization and reduces bond purchases, private markets must absorb larger share of issuance at market-clearing yields rather than central bank-controlled rates.

Debt-to-GDP Over 250% Makes Japan Uniquely Vulnerable

Japan's government debt-to-GDP ratio exceeds 250% according to IMF data, substantially higher than other major economies. United States sits near 120%, Eurozone averages 90%, United Kingdom approximately 100%. This extreme leverage means Japan faces disproportionate sensitivity to interest rate changes compared to peer economies.

The vulnerability stems from debt stock, not flow. Japan runs modest primary deficits in recent years, meaning government spending excluding interest payments roughly matches revenue. However, the accumulated debt stock creates enormous refinancing requirements. Japan must roll over trillions in maturing bonds annually while issuing new debt to cover deficits and interest payments.

At 0% rates, this refinancing posed manageable challenge. At 2% rates, the mathematics shift dramatically. Consider simplified example: ¥1,200 trillion debt at 0% costs nothing to service. Same debt at 2% costs ¥24 trillion annually—roughly 4% of GDP devoted purely to interest expense. This crowds out other spending or requires tax increases that dampen economic growth.

Banking System and Insurance Companies Face Mark-to-Market Losses

Japanese banks and insurance companies hold massive JGB portfolios acquired during decades of yield curve control and quantitative easing. When yields rise, bond prices fall inversely, creating mark-to-market losses on existing holdings. The magnitude depends on duration—longer maturity bonds experience larger price declines for given yield change.

Japanese banks held approximately ¥200 trillion in JGBs as of September 2025 according to Bank of Japan flow of funds data. Insurance companies and pension funds hold additional ¥300+ trillion. A 100 basis point yield increase on 10-year duration portfolio creates roughly 10% price decline. Applied across holdings, this represents tens of trillions in mark-to-market losses.

Most institutions classify JGB holdings as hold-to-maturity, avoiding immediate recognition of mark-to-market losses. However, rising yields still impact institutions through multiple channels. New lending competes with risk-free government bonds now offering 2%+ returns. Banks must offer higher deposit rates to retain funding. Net interest margins compress as funding costs rise faster than asset yields adjust.

Global Carry Trade Dynamics Reverse When JGBs Offer Yield

For decades, Japanese government bonds offered negative or near-zero yields, making them purely collateral assets rather than return-generating investments. Institutional investors borrowed yen cheaply, sold JGBs to raise funds, deployed capital into higher-yielding global assets. This carry trade provided consistent funding for risk asset purchases worldwide.

When JGBs yield 2%+, the calculus changes fundamentally. Japanese investors can achieve positive real returns domestically without currency risk or foreign asset volatility. The incentive to deploy capital abroad diminishes. Repatriation flows accelerate as maturing foreign investments return to domestic JGB purchases rather than reinvesting abroad.

The scale of potential repatriation matters tremendously. Japanese institutional investors hold approximately $4 trillion in foreign securities according to Ministry of Finance data. Even modest percentage repatriation—say 5-10% annually—represents $200-400 billion in capital flows away from foreign assets toward domestic bonds. This withdrawal of liquidity pressures asset prices globally, particularly in markets that benefited from Japanese capital inflows during the zero-rate era.

Rising Inflation Expectations Drive Yields Higher

Japan experienced persistent deflation or near-zero inflation for three decades following 1990s asset bubble collapse. This deflationary psychology kept inflation expectations anchored near zero, allowing ultra-low nominal yields. Recent years showed meaningful shift as inflation rose above 2% for sustained periods.

Core CPI excluding fresh food averaged 2.5-3.0% through much of 2024-2025 according to Statistics Bureau data. While inflation moderated from 2023 peaks, it remains elevated relative to historical Japanese norms. Wage growth accelerated as labor market tightened, with spring wage negotiations yielding largest increases in decades. These dynamics suggest inflation expectations shifting higher on structural rather than temporary basis.

When inflation expectations rise, bond investors demand higher nominal yields to maintain real returns. If inflation runs 2.5% and investors target 0% real yield, nominal yields must reach 2.5% minimum. Current 2.10% yield suggests markets price approximately 2% inflation expectations with minimal real yield premium. Further inflation acceleration would push yields higher still.

Bank of Japan Caught Between Fiscal and Monetary Imperatives

The Bank of Japan faces impossible trilemma. Supporting JGB market requires massive bond purchases keeping yields suppressed. But yield curve control proved unsustainable as inflation rose and policy divergence with other central banks widened. Normalizing policy allows market-based price discovery but threatens fiscal sustainability and financial stability.

The central bank attempted gradual normalization throughout 2024-2025, raising policy rate from negative territory to 0.50% and widening yield curve control bands before eventually abandoning framework. Each step triggered market volatility and yen weakness, forcing periodic interventions and policy adjustments. The path forward remains unclear—full normalization threatens government finances, but maintaining artificial suppression risks credibility and currency stability.

Global Implications Extend Beyond Japan

Japan's JGB market represents third-largest government bond market globally after United States and China. Sustained yield increases and reduced Bank of Japan purchases remove significant source of global liquidity. When major central bank shifts from massive QE to quantitative tightening, global financial conditions inevitably tighten regardless of other central banks' policies.

The carry trade unwinding creates additional global spillovers. Yen-funded positions financed global risk asset purchases for decades. Rising JGB yields accelerate this unwinding by making domestic Japanese assets more attractive relative to foreign alternatives. The capital repatriation pressures risk assets worldwide, particularly those that benefited most from Japanese capital flows.

Implications for Crypto and Risk Assets

Rising JGB yields matter for crypto markets through multiple transmission channels. Higher risk-free rates globally reduce relative attractiveness of zero-yielding assets like Bitcoin. When Japanese government bonds offer 2%+ returns, investors require higher expected returns from riskier assets to justify allocation. This repricing typically occurs through multiple compression rather than fundamental deterioration.

The liquidity channel matters equally. Japanese institutional capital supported risk asset purchases globally, including indirectly funding crypto market growth through VC investments, exchange liquidity provision, and institutional participation. Repatriation flows withdraw this liquidity even absent fundamental crypto developments, creating selling pressure independent of adoption metrics or technological progress.

The correlation between Japanese yields and crypto prices warrants monitoring. Previous Bank of Japan tightening episodes correlated with crypto market weakness through broader risk-off dynamics. Sustained JGB yield elevation likely produces similar pressures through 2026 as markets adjust to structurally tighter global liquidity conditions.

Japan's 10-year government bond yield reaching 2.10%—highest since 1999—represents more than technical market move. It signals potential end of extraordinary monetary experiment that defined global finance for quarter century. With debt exceeding 250% of GDP, Japan faces arithmetic challenges that don't resolve easily once yields normalize.

The global implications extend beyond Japan's borders. Reduced Bank of Japan bond purchases withdraw liquidity. Carry trade unwinding repatriates capital. Banks and insurers face balance sheet pressures. Risk assets globally reprice for environment where Japanese government bonds offer genuine yield rather than serving as pure collateral.

Whether current yield levels prove sustainable or trigger policy reversal remains uncertain. But the direction is clear—the era of costless Japanese government debt is ending. Markets built on assumptions of permanent zero rates must adjust. That adjustment process rarely proceeds smoothly, and crypto markets should expect volatility as repricing unfolds. When the world's most manipulated bond market starts to break, all risk assets feel the impact.

.png)